Evolution and Bridging the Sustainable Finance Gap

In a process of “guided evolution”, the transformation to a more sustainable economy will be driven by self-referential systems where the usual preference for long-term policy predictability can become counterproductive. Government policy will instead zig-zag to reflect society’s changing sustainability knowledge, technology and needs. We can bridge the sustainable finance gap, but only if finance is delivered in a flexible way that can react to this process of change.

US$3.9 trillion: that was the latest OECD (2022) estimate for the annual sustainable finance gap – the difference between current and necessary spending to meet the UN Sustainable Development Goals (SDGs).

The range of needs covered by this simple total is vast, as are the different estimations of the financing gaps for such needs when taken in isolation. To provide some examples, the OECD reckons that almost US$1 trillion is needed per year for biodiversity protection and enhancement. At the same time, it has been estimated that that there is an Ocean Finance Gap of around US$300 billion per year, and that we need US$1.4 trillion per year for investments in renewable energy and electrification.

Work by many governmental and non-governmental institutions is helping to identify and quantify these gaps. Yet, the variety of estimates and their magnitude should be sufficient to highlight the urgency of the problem, and consequently the need to address it systemically.

At first, US$3.9 trillion seems like an impossibly large number. But these trillions seem more achievable when measured against the world’s gross domestic product of around US$100 trillion. Raising this amount would also seem like a priority when the possible costs of failing are considered.

And standing still – continuing with “business as usual” – has appreciable costs, particularly on a cumulative basis. According to an analysis by insurance broker AON, natural disasters caused US$ 313 billion global economic losses in 2022 already, of which less than half was insured. Considering that half of global GDP has been estimated to be dependent on nature and its ecosystem services, it is easy to foresee how climate change impacts will become more acute in the future.

So why is money not flowing across to fill this financing gap?

Providers of sustainable finance face a range of obvious problems, as have providers of finance generally. These boil down to the following: can projects be made to be economic viable, given their size, associated risks, their physical location and so on? Assessing all this – and managing the resulting costs of uncertainty – has been central to financing for many centuries.

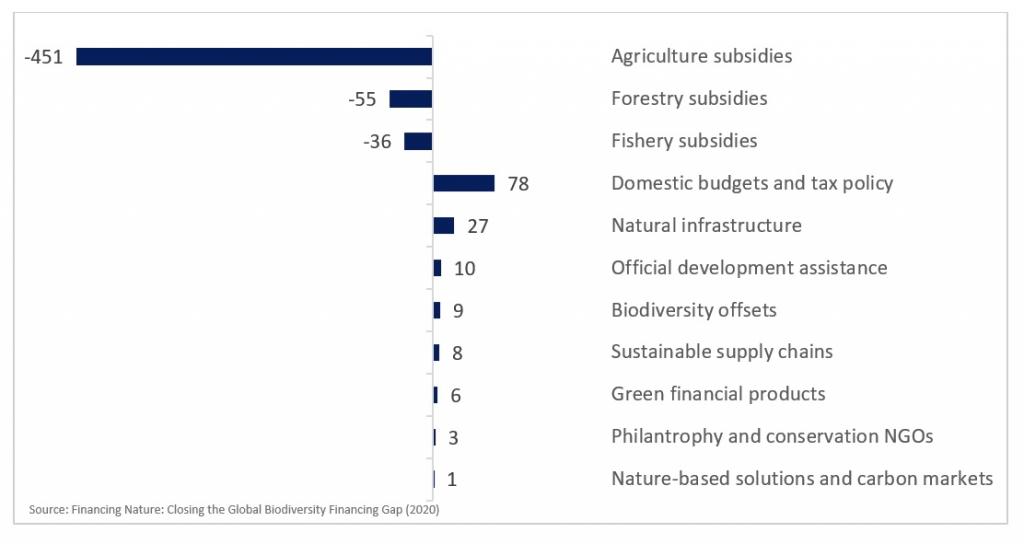

Raising finance for sustainable finance is made more difficult, however, by the role of government – current and future. At present, government finance has effectively “unlevelled” the level playing field. According to a 2019 estimate, for example, the amount of environmentally harmful agricultural subsidies alone was $451 billion per year, more than three times the amount of all estimated financial flows toward biodiversity conservation (see chart below).

The level of government intervention will remain high, whatever individual governments’ inclinations, compared to previous economic transformations e.g. the 17th/18th century industrial revolutions. This will simply reflect the much bigger role governments have in contemporary economies.

But how governments should best get involved in the current sustainable transformation is still uncertain. The challenges are vast and may come at costs to governments themselves.

Governments (and electorates) are well aware that all periods of economic and policy change involve winners and losers. But in most previous periods of change, economic pressures have been the driver: “loser” sectors are clearly going to lose (e.g. hand looms vs. mechanised looms), or resources are clearly running out (e.g. wood supplies to power early industrialisation, before switch to coal). The need for change has been obvious and immediate.

This time around, the ultimate drivers of change (i.e., human survival) in the sustainable are irrefutable but the immediate need for change will be less obvious to many participants and involve significant negatives. In the energy transition, for example, it will require reducing existing technology which still seems highly effective (e.g., petrol engines) powered by resources which are seemingly infinite in availability (oil). The immediate economic drivers for change may be less obvious.

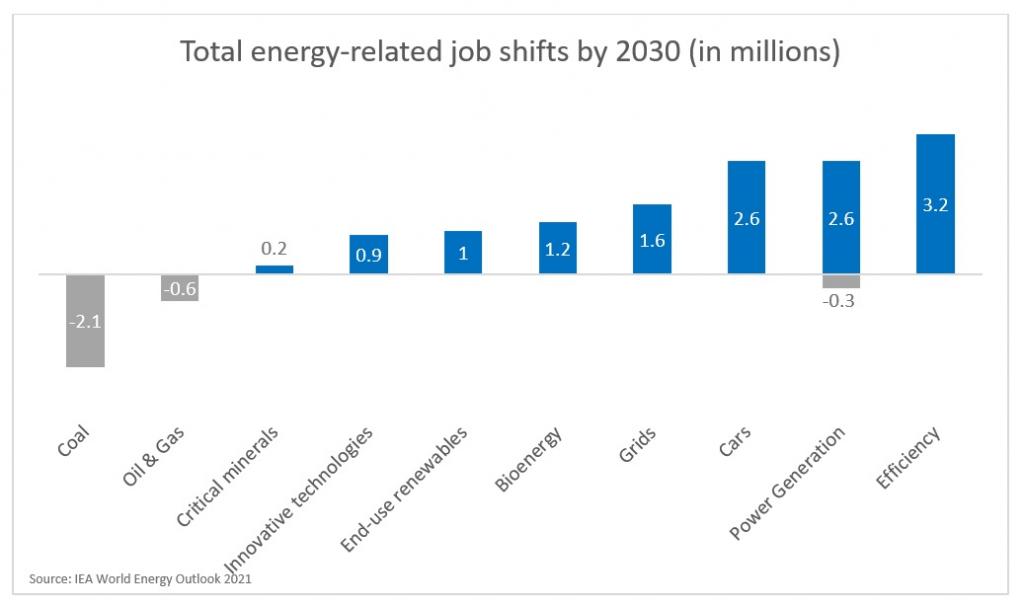

Change will also involve massive shifts in employment (the chart below illustrates for the energy sector), with many losing out and potentially finding it difficult to find employment in new emerging sectors. Governments, to a greater extent than in previous transformations, will be called upon to mitigate these costs so that no one is left behind.

Governments may therefore be tempted to row back on long-term commitments. It is already possible to see this in the energy sector: according to OECD (2022), financial support for fossil fuel production and consumption is back and higher than pre-Covid levels.

Underlying these problems are the two fundamental ways that the sustainability transition differs from previous economic transformations.

First, economic development can no longer be of an additive nature. The success of previous transformations such as the industrial revolution or the post-World War II boom were measured simply in terms of economic expansion. Now success is itself a balancing act: the aim is to transform the existing economic system to be ecologically sustainable and, and the same time, to limit the social and economic costs of transformation to maintain prosperity. Success may therefore be difficult to measure, at least from the perspective of the affected populations.

Second, the role of time itself has changed. Previous transformations always benefited from the inheritance and thus accumulation of knowledge: in a sense, the pace and time scale of the transition was determined by the development and implementation of technology. Now we also have an external “hard deadline” in terms of mitigating the effects of the Triple Planetary Crisis (climate change, pollution, biodiversity loss) before they make existence difficult. The pace of change is being driven by factors that are not immediately under our control.

Policymakers therefore will have a difficult time in finding a balance between current pain (associated with the sustainability transition process) and future gain (survival at acceptable levels of economic comfort). They will operate on a spectrum between:

- Proactively intervening now, with the hope mitigating future social and economic pain, but with immediate political risks.

- And reactively responding only when things get worse (which could be much more long-term costly in economic and social terms, but politically easier now).

We can also be certain that the transition process will not be smooth in terms of speed or direction: it will zig-zag as our technology and knowledge of the natural system improves. Transformations like these must be seen as self-referential systems: we are both shaping and in turn being shaped by economic and social factors.

So, as we try to shape the sustainability transformation by implementing policy measures, they will have a socioeconomic impact on us. The key is to find a way of managing this interplay between creative destruction and destructive creation. Academic studies – for example Strohmaier et al., 2019 – are now identifying the key factors here.

For me, the key question is how we should best encourage this process and generate finance for it, given that it needs to be both non-additive and achieved reasonably quickly (meaning that we cannot wait for technology to perfectly meet our needs.)

I think we should see this as a case of guided evolution.

Governments need to intervene to temporarily encourage a change of direction. To fulfil this need, they need to identify certain trigger points and apply specific policy tools to address them. They also need to set some self-imposed limits on their activities: while it is tempting for everyone to ask the state for short-term and direct interventions e.g. via subsidies, these may only address local problems and the overall impact of such support will be dissipated and quickly evaporate.

Governments need to understand that we are now facing a systemic and not a local crisis. It is therefore essential for them not to focus on localised palliative care, but to look at the challenges systematically and to push change in the right direction through long-term systemically oriented measures, creating new framework conditions for a better adaptation to future changing circumstances. What this means, in effect, is that a government will have always to be on its toes.

Providers of sustainable finance need to get used to this process of change. This will require accepting some developments that appear counterintuitive. Traditionally, the orthodoxy has been that transformation is dependent on government policy that is guaranteed for the long term: economic transition is seen as a long-term problem.

But in this uncertain situation, where changing knowledge is continually forcing us to reappraise, pursuing fixed long-term policy may be counterproductive. There is no point encouraging financial flows into areas which we now realise are no longer the best way to solve our problems. The danger is that policy becomes an expensive hindrance not a help (and we should not pretend that the distortions around conventional subsidy problems will not be replicated in long-term sustainable finance support.) Financial market development will respond to policy, so we need to get this right.

Focusing instead on “trigger points” will require us to be much nimbler and to abandon subsidies and other incentives for particularly technologies etc. when they no longer make sense. (Something that can be politically difficult, when economic actors become accustomed to the financial support.) We should also be prepared to change individual sustainable finance markets if they are no longer delivering benefits: as in previous industrial transformations, finance may need to flow through unexpected ways.

Evolution, as we know, weeds out losers to find species that can survive: likewise, policy needs to help us find workable solutions, rather than persist with ones that no longer work. In the natural world, we also know that the development of adaptive parental protection (embryo retention/eggs) helped give amniotes the edge. But natural development also suggests that the timing/extent of such protection will vary in terms of benefit over time. The lesson is that subsidy/protection programmes for transition technologies will need to vary over time: we have to be flexible. In fact, I think the biggest problem for bridging the financing gap is to how to ensure that finance evolves as the transition evolves – to deliver large amounts of finance in a way that is flexible and reacts to change.

Photo by Klas Tauberman